Contact

Contact

Find an agency

Find an agency

Close

Close

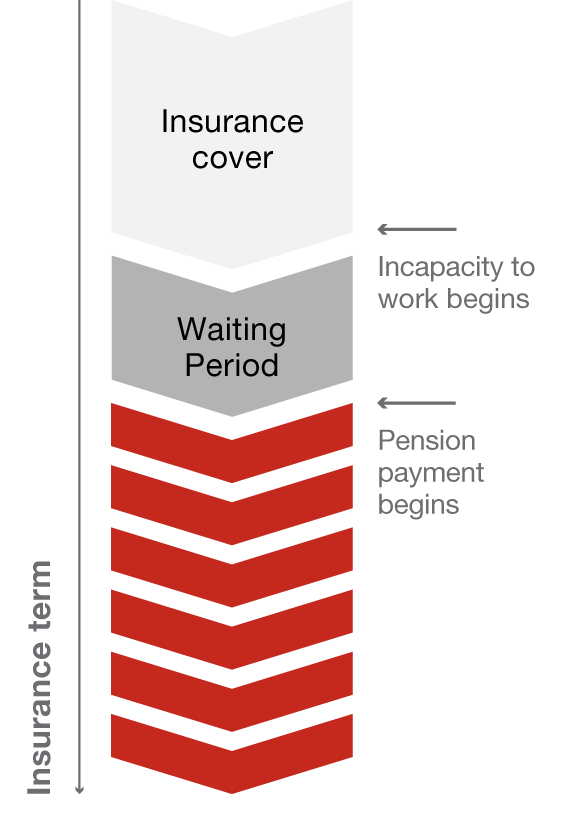

So you can maintain your standard of living.

- Loss of earning capacity due to illness or accident

- Individual choice of amount of pension

- Tax advantages with premiums saved in pillar 3

- Including premium exemption: Premiums covered in emergencies

- No premium increases during the first 5 years