Contact

Contact

Find an agency

Find an agency

- Advice

- Life events

- Insurance

- Services

- Report a claim

-

-

-

Close

Close

First home

The invisible gap in your protection.

A silent cost trap in your home that can end up costing you a fortune.

A CHF 30,000 loss occurs, CHF 18,000 is reimbursed – the rest? Your problem. That’s why it’s important not to choose a sum insured that is too low for your household contents. Otherwise, you are underinsured. In the event of underinsurance, you will not receive the full amount of the loss. We explain why this can happen.

Do you have a clear overview of your household contents insurance?

Your home grows – with memories, new purchases, favourite items. But does your household contents insurance grow with it? Many people only realise after a claim that their cover is no longer sufficient. Our example shows how underinsurance occurs – and how you can avoid it with ease.

Think of everything that matters to you.

All your belongings have a value – and this should match the sum insured in your household contents insurance. People often forget to take their entire inventory into account, to include new purchases, or they simply misjudge the total value. If your sum insured does not correspond to the actual value of your household contents, you are underinsured. In the event of a claim, this means you will only receive part of the loss – proportionate to the relationship between the insured and the actual value. Our calculation example shows what happens when your insurance cover is insufficient.

A sum insured that is too low can become expensive in the event of a claim.

A practical example:

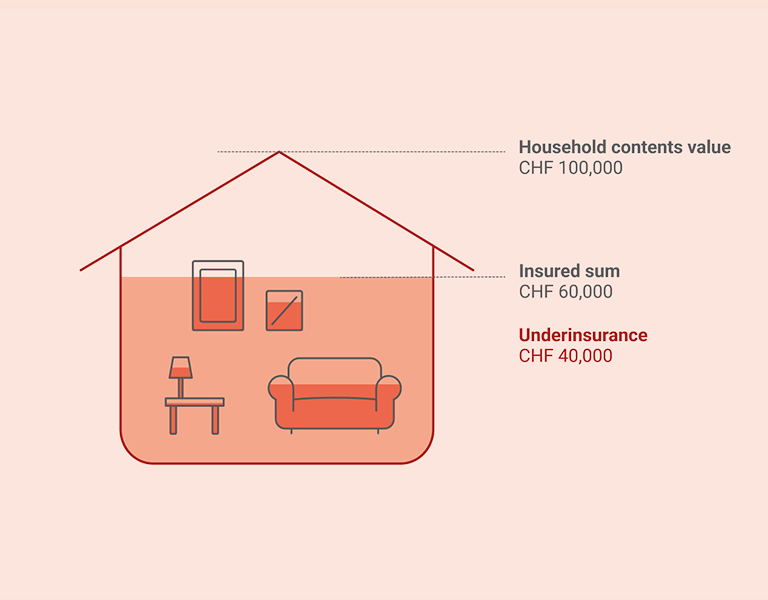

Three years ago, you took out a household contents insurance policy and specified a value of CHF 60,000. Since then, you have bought new furniture, a luxury watch, an ebike, and inherited jewellery. As a result, the total value of your household contents has increased to CHF 100,000. This means you are now only 60% insured.

That’s not good. If only 60% of your household contents are insured, the insurer will also cover only 60% of any loss. Suppose burglars steal various valuables worth CHF 30,000. Due to underinsurance, the loss would not be fully covered.

In plain terms: if your household contents are worth CHF 100,000 but only CHF 60,000 are insured, you will receive just CHF 18,000 for a loss of CHF 30,000. You pay the remaining amount yourself – even for small claims.

Good to know: We recommend that you regularly review your sum insured. Over the years – or when moving to a larger home – the value of your household contents often increases. When this happens, it is important to adjust your sum insured accordingly.

Other suitable insurance products